On the day of completion, a few outstanding items get finalised. First of all, the buyer’s solicitor pay the remainder of the sale price of the property to the seller’s solicitor after having received the mortgage advance from the bank and any outstanding sums from the buyer. Upon receipt of the remaining funds, the seller’s solicitor releases the keys for the property to the buyer through the selling agents. The buyer can then begin moving in. If you are in a chain, it may take the whole day for all transactions to complete as all funds need to move along the chain. In any event all sellers in the chain need to vacate their property in the morning and await receipt of the keys for the property they are buying. This means that there may be a gap of a few hours where everyone has moved out and has all their belongings in removal vans and await the keys to their new home.

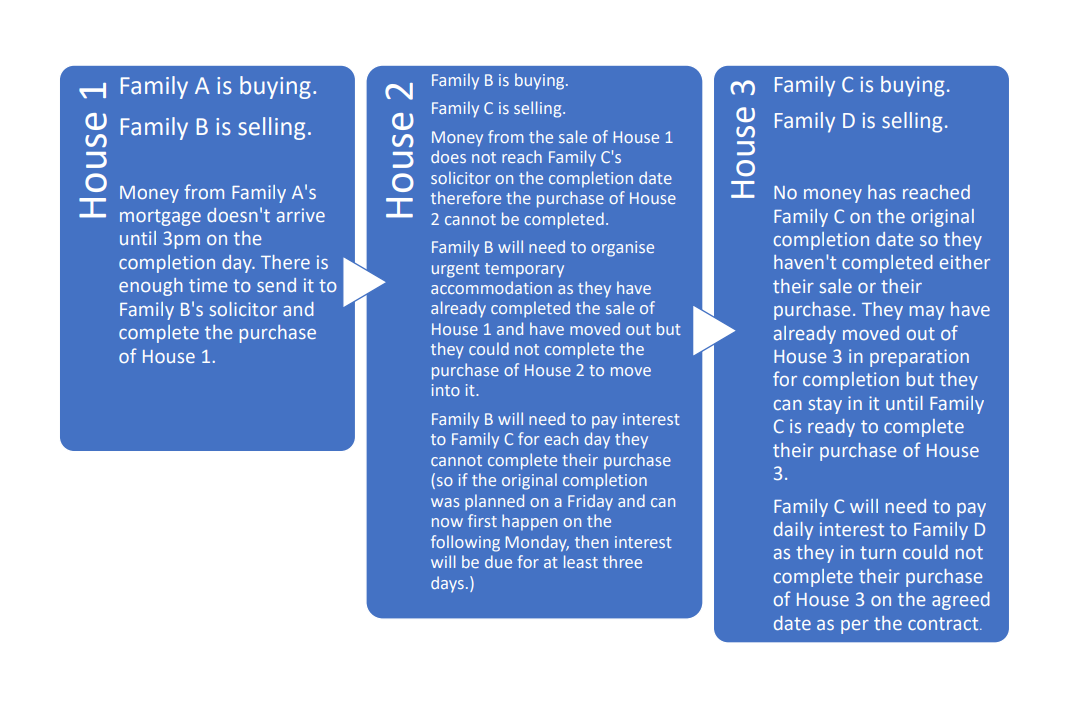

The date of completion does not change after the exchange of the contracts unless in exceptional circumstances. For example, if someone’s mortgage funds get delayed this may mean that the last transaction in the chain (or the last few) may not be able to complete on that day. If a seller in the chain manages to complete their sale but do not have time to complete their purchase, they will need to stay at a hotel or with friends and relatives until the next working day when they can complete their purchase. Their belongings will need to stay with the removal company as well. in such cases there is a breach of the contract so the defaulting party (usually the buyer) will need to pay interest and potentially compensation to the seller. Below is a diagram which explains a delayed completion:

You can use Appendix 8 from Part One of the book “How to buy your first home in England (and Wales)” to enter details about your chain and make it easier to track progress and developments.

You can also use Appendix 13 from Part One of the book “How to buy your first home in England (and Wales)” to create own to-do list for this part of the process.

Solicitors should make sure they explain the consequences of a delayed completion to their clients.

Insurance policies after completion

Apart from advising you on the various mortgage options, mortgage brokers can also recommend you take out some protection insurance policies following completion of your purchase. Below is a list of the main ones with short details about each:

Contents insurance – covering your belongings such as furniture, jewellery, electronic devices, carpets, clothes against fire, damage from flooding, accidents and theft. Most commonly it is offered as part of the building insurance you must take out upon exchange of contracts.

Life insurance – in case of death, the policy will pay out a lump sum to your relatives to use as they find appropriate.

Private Health insurance – quick access to medical services, specialist medication and procedures, private hospitals, choice of doctors and hospitals.

Accident insurance – against falls, cuts, burns, road traffic accidents, bites and drowning – it covers urgent care expenses, hospital stays, medical examinations and others in cases of serious injury or death caused by an accident. Most commonly it is offered as part of your car insurance and it covers not only the vehicle but also the driver. If you are unable to work due to the injuries after the accident, the policy would also cover loss of income compensation.

Business insurance – against client claims, damage to tools or equipment related to your business, human errors. There are many types depending on the nature of your business – public liability insurance, product liability insurance, professional indemnity insurance, employers’ liability insurance, buildings cover, contents and stock cover, theft of takings, business interruption, cyber insurance and legal expenses.

Income protection – in case you are unable to work for a long period of time due to illness. It pays out about 85% of your income before tax until you can go back to work or retire.

Critical illness – insures against serious conditions such as cancer, heart attack or stroke, multiple sclerosis, Parkinson’s disease, Alzheimer’s disease, organ failure, loss of limbs and others. It pays out a lump sum to use as you wish, for example medical expenses, monthly expenses, income replacement or others.

Mortgage protection – there are two types – mortgage life insurance policy, which covers your monthly mortgage instalments in case of death, and mortgage payment protection insurance policy, which covers your monthly mortgage instalments in case you are unable to work due to illness or accident.

You can use Appendix 3 from Part One of the book “How to buy a property in England and Wales” to compare the different insurance policy products you have been quoted in order to decide which one is best for you.

If you need to discuss the various insurance options with a professional, we are recommending Georgi Petrov from Umbrella Protect. He has consistently been receiving positive reviews from his clients and is widely recommended on social media. Below are his contact details:

Georgi Petrov

Protection Adviser

07522115859

Georgi.petrov@umbrellaprotect.co.uk

You can use discount code A-King when contacting Georgi to take advantage of the best rates and service at Umbrella Protect.

If you are buying for the first time and have been living in rented accommodation so far, the first unpleasant surprise you will face in your first year as a homeowner are the bills and expenses linked to the general running of the household. You can use Appendix 14 from Part One of the book “How to buy your first home in England (and Wales)” to create and structure your own household budget following your purchase.