Stamp Duty Land Tax (SDLT)

This is the tax payable upon the purchase of any type of land or property over a certain value – above £125,000 for residential properties and above £150,000 for non-residential property such as land to build.

The tax return needs to be submitted to HMRC and the tax due needs to be paid within 14 days of completion. Your solicitor will draft the return for your approval in advance, possible after exchanging the contracts and will submit it on your behalf after completion. If not submitted or paid within 14 days, late filing penalties and intertest will start accruing.

SDLT is calculated by sectioning off the purchase price in the following way:

- There is no tax due for the first £125,000 (for a residential property).

- From £125,001 to £250,000 the tax will be 2% of this part of the price. For example if the property price is £130,000, the tax payable will be 2% of the £5,000 which is above the £125,000 threshold, so £100.

- From £250,001 to £925,000 you will pay 5% calculated on this part of the price.

- From £925,001 to £1.5 million you will pay 10% and if the price is above £1.5 million, the tax will be 12% of the amount which is above £1.5 million.

Here is a link to the official SDLT calculator.

If you will be an owner for the first time, you will be eligible for first time buyer relief. This means that there will be no tax payable if the property is under £300,000 and if it is between £300,001 and £500,000, then it will be 5% from the part of the price above the £300,000 threshold.

There are other reliefs you may be able to benefit from which is best to discuss with your solicitor or tax adviser. You can read more about them on this page.

If you are buying your home in stages under the Shared Ownership scheme, you don’t need to pay any tax until you reach 80% equity in the property and no part you have bought is worth more than the £125,000 threshold. Under this scheme you can either chose to pay tax every time you buy another share, so to pay the tax in stages, or you can choose to pay the tax on the full property value upon your initial purchase of shares (market value election). This means that you will have paid the full tax on the current value of the property, which will otherwise be raising and not on higher value when you buy more shares further down the line. If you choose this option you will not need to pay any further tax when you buy any of the remaining shares.

If you are buying your second or additional property, you will also pay a 3% surcharge on top of the tax due as calculated above. If you sell your first property in the same time as buying the second one, then you will not pay the surcharge as you will not end up owning more than one property. If you sell your first property within three years of purchasing the second one, then you can apply for a refund of the surcharge.

From 1st April 2021 non-residents of the UK will be liable to pay 2% additional tax when buying a residential property above £40,000 even if they are eligible for first time buyer relief. This additional tax is also charged to companies which are set up in the UK but controlled by non-residents of the UK. Non-residents are people who haven’t resided in the UK at least 183 days (about 6 months) in the 12 months before the purchase. Once non-residents have lived in the UK for more than 6 months out of the 12 months before or after completion of the purchase, they can apply for a refund of the 2% additional tax.

This topic is as wide as it is complex as it depends on each individual’s circumstances. Your solicitor will draft the return based on the most basic calculation of the tax. If your circumstances are very complicated they may refer you to a tax specialist for additional advice.

Land Registry

The Land Registry is an official record since 1862 in England and since 1875 in Wales. It contains information about more than 24 million properties. Initially, the Register included only voluntary registrations, but since the early 1990s, all counties in England and Wales have adopted the practice of mandatory registration of certain property transactions, such as sales.

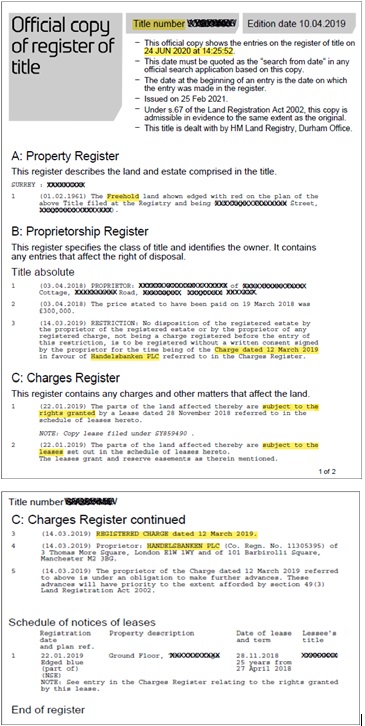

The Register is public and electronic. When an official copy of the title for a property is needed, the Land Registry issues an excerpt of the official register which is accurate as at the date and time it was issued. Below is an example of a title deed.

Every registered piece of land, regardless of whether there is a building on it or not, has a unique identification number called title number. Every title deed contains three parts – A. Property register; B. Proprietorship register; and C. Charges register. We have explained what these contain in more detail in chapter 2.2.1 of Part One of the book “How to buy your first home in England (and Wales)”.

The official plan of a property is the other important part of the official documents. It provides an approximate indication of the location of the property, but it does not define its boundaries. It is important for the official title plan to be checked by the buyers to make sure it matches the location of the property they have viewed. The buyer’s solicitor will also check the plan to make sure it is the same in all official deeds, documents and searches.

The Land Registry needs to be notified of each purchase, as well as every change in the information contained on the title deed, so that the record is up-to-date and these changes become official. This is being dealt with by the buyer’s solicitor who will submit an application to register the redemption of the seller’s mortgage, the transfer of the property from the seller to the buyer and the registration of the buyer’s mortgage. Once the registration is completed, the Land Registry will issue an updated title deed and will send it to the buyer’s solicitor.

Depending on the type of the property and the type of transfer, the registration process may take from a couple of weeks (for a standard existing freehold property) to more than a year (for a new build flat for example).

The Land Registry has recently implemented a new registration portal which deals with registrations a lot quicker but this is still only limited to certain types of applications at the moment.

Registration fees vary according to the value of the property and the type of transfer for example is it a whole title which is being transferred or is it part only of the seller’s land which would be the case of a new build property in an estate. Here is a link to the Land Registry fee calculator.