Before deciding to buy a property (or indeed taking out any kind of loan) you must ensure your credit history is clean. If it is not, bank would still lend you a mortgage but only specialist lender would and they would offer you higher interest rates. You can check your credit file online at sites such as Experian, Equifax and Noodle. A clean financial past would help make the mortgage application process and therefore your purchase go smoother.

You can use Appendix 1 from Part One of the book “How to buy your first home in England (and Wales)” to tick off different steps you can take to improve your credit score.

About the deposit

When buying a house, there are two types of “deposit” which are being mentioned and talked about by agents, mortgage advisers and solicitors. Very often the terms are being used interchangeably which can be confusing. Below we have explained the difference.

1. The 10% deposit you need to exchange contracts on your purchase – that’s how much is required by Protocol regardless of whether you have more saved and are taking out lower mortgage or you have less saved and are taking our higher mortgage. In order to exchange contracts, you will need to have sent 10% of the purchase price to your solicitor’s firm bank account, unless the seller has agreed in advance to accept a lower deposit.

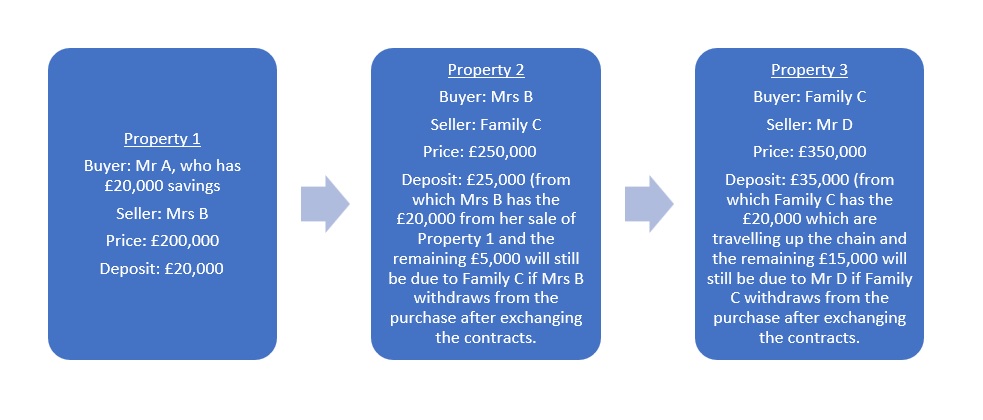

IMPORTANT: Even if the seller has agreed to accept less than 10% deposit upon exchange of the contracts, if you fail to complete your purchase, you would still owe the balance to 10% to the seller. A lower deposit is usually acceptable when there is a chain and the same deposit from the bottom of the chain travels up the chain. Below is an example of this.

2. The “Deposit” for your mortgage – it is widely referred to as a deposit as well however it is just the percentage of the finance which you will need to have as the banks would normally only finance up to 95% of your purchase based on your income. The mortgage offer is based on the assumption that the buyers have the remainder needed to complete the purchase. The more “deposit” you have available, the bigger your share in the property would be (your equity) therefore the bank’s share would be less which means lower risk for them and therefore lower interest rate on the loan.

So by Protocol, you must have and sent your solicitor 10% of the purchase price as a deposit to exchange the contracts (unless the seller has agreed to accept a lower amount) regardless of how much financing you have requested from the bank.

How much deposit do we need to have saved?

You need to have available at least 5% from the value of the property you wish to buy in order to obtain a mortgage from the banks. The more deposit you have available, the lower the interest rate on the mortgage would be.

There are a few government schemes which help fund the purchase of your first home which only require a 5% deposit from the buyers – First Homes, Rent to Buy, Help to Buy: ISA, Lifetime ISA, Help to Buy: Equity Loan, Help to Buy: Shared Ownership, Older People’s Shared Ownership (OPSO). We have gathered more information about these in chapter 5.4 of Part One of the book “How to buy your first home in England (and Wales)”.

The time it takes to save the deposit is individual for everybody. Some lucky sods just get a lump sum as a gift from a relative while others save for years. You can find more ideas about how to save quicker in chapter 5 of Part One of the book “How to buy your first home in England (and Wales)”.

You can use Appendix 2 of Part One of the book “How to buy your first home in England (and Wales)” to complete your own balance sheet of income and expenses which will give you a better idea of where you can save from and what expenses you can cut off.

Source of funds

Source of funds checks are becoming ever more in-depth and almost invasive. Checking the origin of the money you use for a property purchase is a main step of your purchase process regardless of whether you have the money from savings, sale of a property or a gift from a third party. The real estate market in the UK is a very attractive area for criminals to try and launder their crime proceeds and that is why the checks in this sector are most comprehensive and to the highest standard.

The source of funds checks are done at least twice in the process – once by your bank before issuing the mortgage offer and another time by your solicitor before they confirm they would take on your purchase. The latter is a lot more detailed as the lawyers as well as the firms they work at bear criminal liability if they fail to demonstrate that they have taken all reasonable steps to confirm the money used for each property purchase does not come from any criminal activity. Moreover, the banks rely on the solicitor’s check rather than their own so solicitors are responsible not only in front of the banks but also in front of the regulatory bodies.

From solicitor’s point of view, we need to understand and see proof of the origin of the money used for the purchase and not just a statement that it is in the buyer’s account. We literally need to find out its initial source and see evidence of it.

If you are not sure how to demonstrate the origin of your deposit then it is best to ask your own solicitor as each firm has own policy as to what constitutes “reasonable steps” and enough evidence.

If your solicitors are not happy with the evidence you provide or if they find a reason to believe your funds come from any type of crime including misuse of social benefits, tax evasion and so on, they will not only refuse to act for you but may also report you the relevant authorities.

Are you a first time buyer?

It is good to establish whether you are a first time buyer or not at the beginning of the process.

“First time buyer” is an informal term used in a number of places throughout the process of buying a property. It is intended to segment those people who intend to obtain their own home and haven’t had the chance before so it is perhaps more accurate to use “first time owner” as they may have had a gifted or inherited property before, which was not purchased so essentially they are currently buying for the first time but have owned a property before which is not what the government schemes are intended for.

Whether you are a “first time buyer” or not is also important in order to determine whether you are eligible for the first time buyer relief in relation to Stamp Duty Land Tax.

We have written more about who is classed as a first time buyer and how this affects the tax duty and the purchase financing in chapter 5.3 of Part One of the book “How to buy your first home in England (and Wales)”